AI Is the Fourth Industrial Revolution: What It Means for Investors

Disclosure: This article contains affiliate links. If you register through our links, we may earn a commission at no extra cost to you.

Every major industrial revolution was obvious in retrospect and bewildering from inside it. The cotton mill owners of 1790 did not recognise themselves as participants in a structural transformation of the global economy. They were solving immediate problems: labour costs, distribution, competition. The transformation happened around them, through them, and despite them.

We are roughly five years into the fourth version of this story. The AI revolution is not a software upgrade or a productivity trend. It is a structural reorganisation of how economic value is created, where it concentrates, and which assets and capabilities will matter most in the decades ahead. The infrastructure race is already underway. The positions are not yet set.

This article covers the physical and financial infrastructure of the AI economy: who controls the compute layer, why energy has become the real constraint, how the US-China geopolitical competition is reshaping the global technology order, and what it all means for digital investors who want to position for the shift rather than read about it after it happens.

One observation from those closest to this transition is worth stating plainly at the outset: AI is no longer optional for any organisation that intends to remain relevant. That may sound like marketing copy. The evidence suggests it is simply a factual description of where competitive pressure now sits.

We Have Been Here Before

The pattern across industrial revolutions is consistent enough that it functions almost as a template. Each revolution was driven by a new infrastructure layer that made the previous generation of capital and labour arrangements obsolete, concentrated enormous wealth among those who controlled the new infrastructure, and created conditions for new application-layer industries that the infrastructure builders did not themselves anticipate.

What the table does not show is the sequencing within each revolution. In every case, the infrastructure builders won first and fastest, not the application builders and not the end users. The railroad barons did not profit primarily from the goods shipped on their lines. They profited from the lines themselves, years before meaningful commerce moved across them. Carnegie did not profit primarily from the things made with steel. He profited from controlling the steel.

The fourth industrial revolution is following this pattern with unusual clarity. The infrastructure layer is visible. The companies controlling it are identifiable. And the window for infrastructure positioning remains open, though not indefinitely. The consensus view that “AI is the fourth industrial revolution” has shifted from provocative claim to near-standard framing among economists and technology leaders in less than three years. The debate has moved to second-order questions: which countries win it, which industries are transformed most completely, and which investors capture value from the shift.

What Makes This Revolution Structurally Different

Capital Requirements Across Industrial Revolutions

Railroad Era

Iron, labour, land

High

Factory Era

Real estate, machinery

High

Internet Era

Fibre, servers, data centres

Very High

AI Era

GPUs, power, cooling, land

Unprecedented

10K+

Specialised GPUs per frontier training run, running continuously for months

$100M+

Hardware cost per training run at the frontier

17

Football fields — Microsoft Iowa data centre footprint

The Structural Difference Most Analysis Misses

Internet Era

Software companies built products on top of infrastructure they did not own, renting compute at commodity rates. The barrier to building was low. Value accrued to application builders.

AI Era

Building at the frontier requires either owning the compute or paying non-commodity rates. The barrier is closer to 19th-century railroad monopoly dynamics than to SaaS economics.

Where Value Migrates as AI Commoditises Software

Compute & Infrastructure Layer

GPUs, data centres, energy, networking

Data & Model Layer

Training data, foundation models, weights

Application Layer

Software products, AI tools, SaaS

As AI reduces the cost of generating code toward zero, value migrates upstream to whatever controls the capability that enables production — compute and data. The revolution commoditises the application tier while concentrating value at the infrastructure tier. This pattern is visible in every previous revolution.

Historical Pattern

Recognising this is what separates structural analysis from surface-level optimism. The revolution commoditises the application tier. It concentrates value at the infrastructure tier. This was true in the railroad era, the electricity era, and the internet era. The AI era is not an exception.

The Infrastructure Layer: Who Controls the Compute

NVIDIA’s Position

H100 · H200 · Blackwell B200

~70–80% market share

80B

Transistors per H100 chip

$40K

Wholesale price per H100

6×

Data centre revenue growth (2023–2024)

TSMC-manufactured at 3nm & 4nm

Among the most sophisticated physical objects produced at commercial scale. Process node leadership is a constraint no competitor can buy their way past quickly.

Data centre revenue: $3B → $18B per quarter

Early 2023 to late 2024. No company in recent history has experienced revenue growth at this speed and scale in a single product category.

CUDA: 15 years of ecosystem lock-in

Essentially all AI training software is built on CUDA. Switching to a competitor’s hardware requires rewriting the entire software stack — a years-long engineering project with significant capability risk during transition.

Analyst Assessment

NVIDIA’s position is described as a moat, not merely a lead. The ecosystem advantage is more durable than any single hardware generation — it would be difficult to replicate even with substantial capital.

vs

Huawei’s Response

Ascend 910B · 910C · SMIC foundry

Export-controlled

~80%

910B performance vs H100 on select benchmarks

7nm

SMIC current process node

3nm

TSMC current process node

Manufacturing Process Node Gap

TSMC

3nm

SMIC

7nm

Multiple technology generations apart. The gap represents years of equipment investment and process development that cannot be shortcut through funding alone.

CHIPS Act export controls forced a parallel ecosystem

Baidu, ByteDance, and Alibaba are building frontier models on Ascend hardware and older NVIDIA chips imported before controls took effect. Progress continues — at materially higher cost and longer timelines.

Design capability is not the binding constraint

The 910C closes the benchmark gap further on certain workloads. The bottleneck is manufacturing, not engineering — a distinction that matters for any realistic timeline assessment.

Realistic Assessment

Export controls have slowed China’s AI development. They have not stopped it. That distinction is important for any honest geopolitical analysis.

The Takeaway

NVIDIA’s hardware lead is real. Its software ecosystem moat is deeper and more durable. Huawei is closing the performance gap by necessity — but the manufacturing constraint cannot be engineered around quickly. The race continues, with the gap measured in years, not quarters.

TSMC and the Chokepoint

The most consequential company in the AI infrastructure race is not one most retail investors can directly access: Taiwan Semiconductor Manufacturing Company.

TSMC manufactures the chips that power NVIDIA’s GPUs, Apple’s processors, AMD’s data centre chips, and essentially every leading-edge semiconductor produced in the world. It is the only company currently capable of manufacturing at 3nm at commercial scale. This concentration creates a geopolitical chokepoint of extraordinary strategic significance: the physical components of the AI revolution depend on a company based in a contested geopolitical territory.

The US CHIPS Act includes investment to bring leading-edge semiconductor manufacturing to American soil. TSMC’s Phoenix, Arizona facility represents approximately $40 billion in committed investment. 4nm production began in 2024, with 2nm planned for 2026. Even when complete, these facilities will represent a fraction of TSMC’s Taiwan capacity. The dependency is reduced by the CHIPS Act. It is not resolved.

The Energy Wars

AI is not, at the infrastructure level, a software problem. It is an energy and cooling problem at historic scale.

The International Energy Agency projects that data centre electricity consumption could reach 1,000 terawatt-hours per year by 2026, roughly equivalent to Japan’s entire national electricity consumption. This is the IEA’s central estimate, not a worst case, and it is driven primarily by AI workloads. Training a single large frontier language model consumes energy roughly equivalent to 300 transatlantic flights. Inference, meaning the deployment of trained models to serve user requests at scale, may ultimately consume more total energy than training, as deployment continues to expand.

The hyperscalers have responded with investment at a scale that reflects how seriously they take the constraint. Microsoft signed an agreement to restart the Three Mile Island nuclear plant in Pennsylvania to power its AI data centres, the first commercial nuclear restart in US history driven by private corporate demand. Amazon has made substantial separate nuclear energy investments for the same purpose. Microsoft, Google, Meta, and Amazon collectively announced over $100 billion in new data centre investment during 2024 and 2025, with energy supply consistently identified as the primary constraint on expansion pace.

Goldman Sachs has projected approximately $1 trillion in AI infrastructure investment over the coming decade. A significant portion of that capital will flow not into chips or software but into power generation, grid infrastructure, and cooling systems. The AI revolution is, at its foundation, an energy revolution. Those who understand the energy cost of AI infrastructure and its implications for adjacent markets are working with a more complete picture than the standard narrative provides.

Key figure: The IEA projects AI-driven data centre electricity demand reaching 1,000 TWh/year by 2026. That is not a rounding error in the global energy system. It is a structural demand shift that is already reshaping investment decisions in nuclear energy, utility-scale solar, and long-duration storage.

The Geopolitical Race

The US Strategy

The United States government has made an explicit policy decision to treat AI semiconductor leadership as a national security priority, not simply a commercial one.

The CHIPS and Science Act, signed in 2022, committed $52.7 billion to domestic semiconductor manufacturing and research. Export controls on high-performance AI chips to China have been progressively tightened since October 2022, with successive rounds closing loopholes identified in previous versions. The strategy is twofold: maintain a technology lead in leading-edge semiconductor manufacturing, which translates directly into AI training capability, and prevent China from acquiring that capability through trade.

The limitation is visible in the TSMC dependency. The US does not yet manufacture leading-edge chips domestically at commercial scale. The CHIPS Act addresses this on a timeline measured in years. During that gap, the US AI lead is maintained through access to TSMC, not through domestic production. The allied fab strategy (TSMC Arizona, Samsung Texas, Intel Ohio) is the correct long-term answer. It is not yet the current reality.

China’s Response

China’s response to the export controls has been systematic. The central government announced a 1 trillion yuan AI investment fund in 2024, directed at domestic semiconductor development, AI research infrastructure, and national compute capacity. The stated policy goal is AI self-sufficiency by 2035.

The practical constraint remains the fab gap. China cannot currently manufacture the chips required for frontier AI training at the cost and performance levels available to US-aligned AI labs. Huawei’s Ascend series represents genuine progress. It does not yet close the performance gap that the 3nm-to-7nm manufacturing difference creates.

China’s advantage is in AI application deployment at scale and in national coordination. Chinese AI labs are training competitive models with constrained compute. Chinese government policy creates deployment pathways that no private company in a market economy can replicate. The assumption that constrained compute means constrained AI capability is not supported by what Chinese labs are actually producing. The gap is real. It is not as large as the chip gap alone would predict.

The Rest of the World

The US-China framing, while accurate as a description of where leading-edge capability sits, obscures a more complex picture. Several second-tier players are making consequential moves that will shape the AI infrastructure landscape of the 2030s.

The UAE has committed approximately $100 billion to AI infrastructure investment, with Microsoft, Google, and OpenAI all establishing major AI hubs in Abu Dhabi. The small state is positioning itself as a neutral AI compute and governance hub for markets that do not want single-point dependency on US or Chinese infrastructure. India’s English-language capability, 1.4 billion population, and deep engineering talent pipeline create structural advantages in AI application development that are compounding from a large base. The UK’s AI Safety Institute is attempting to establish a governance role disproportionate to its compute investment. The EU’s AI Act creates regulatory sovereignty that may prove to be either a competitive advantage or a constraint depending on how the next decade of AI development unfolds.

The biggest cost in this race is not capital. It is fixed thinking: the assumption that the current technological and geopolitical order is stable, and that the competitive advantages visible today will persist without active effort to maintain them. Countries and organisations that update their mental models slowly will find that the infrastructure layer is controlled by others before they recognise the problem.

The Education Layer

The infrastructure of the AI economy is not only physical. It is human. And the human infrastructure being built now will compound over decades in ways that are difficult to model but impossible to ignore.

Hangzhou’s municipal government launched a systematic AI curriculum in 2023 covering children aged 6 to 18. The programme begins with algorithmic thinking and computational logic in primary school, progresses through machine learning applications in middle school, and reaches neural network fundamentals and AI ethics in secondary school. This is not coding education. It is AI literacy designed to produce a workforce capable of directing, managing, and building on AI systems, not merely using them as tools.

China’s national government has mandated AI literacy as a core curriculum element by 2030. The practical implementation is uneven across provinces, but the strategic direction is clear. The workforce being trained today is the AI workforce of 2035 and beyond.

The implication for long-horizon investors is underappreciated. Every employee will eventually manage AI workers in some capacity. The question is which countries are systematically building that capability into their workforces now, before the skill premium compresses. Countries with AI-ready workforces will attract AI investment, produce AI companies, and accumulate AI-era economic advantages at disproportionate rates. The wealth geography of 2035 will differ from today’s. The signals for how are visible in education policy now, if you know to look.

Where the New Wealth Is Shifting

The pattern from previous industrial revolutions, applied to the AI era, produces a sequenced prediction.

Infrastructure builders win first. This phase is already underway. NVIDIA’s market capitalisation trajectory from 2022 to 2025 represents AI infrastructure being repriced by public markets. TSMC’s strategic value has been repriced similarly. The hyperscalers building and operating AI data centres (Microsoft, Google, Amazon, Meta) are seeing infrastructure capex treated as competitive necessity rather than discretionary investment. Goldman Sachs’s $1 trillion infrastructure projection reflects where the capital is going over the coming decade, not where it might go.

Platform builders win second. In the electricity revolution, General Electric built the components that made electrification useful for everyone else, capturing durable value in the transition layer between raw power and end applications. The AI equivalent is whoever builds the dominant model APIs and AI operating systems on which applications will run. OpenAI, Anthropic, Google DeepMind, and Meta AI are competing for this position. The winner of that competition is not yet determined.

Application builders win third and longest. Apple did not invent the transistor or the internet. It built applications on infrastructure and platforms it did not own, and created more durable long-term value than either. AI-native applications are still early. The category has not yet produced its iPhone. The companies that will dominate AI application delivery in 2040 may not exist yet, or may not yet be publicly accessible to most investors.

For retail investors, the practical picture is this. Direct exposure to the infrastructure layer is already priced at significant premiums. Picking winners in the platform layer requires deep technical and strategic knowledge. The application layer is early and high-risk. A fourth path exists: participating in the financial infrastructure layer that the AI economy creates demand for. That layer is digital assets, and the case for it is structural rather than speculative.

AI and Crypto: The Convergence That Matters

Every major industrial revolution created a new financial layer, not by design but because the revolution created economic demands that existing financial infrastructure could not efficiently serve.

The first industrial revolution created the joint-stock company as a mechanism for pooling capital at the scale railways required. The second created the modern stock market and large-scale corporate debt. The third created venture capital as a funding mechanism for technology companies with no physical assets. Each financial layer was not invented to serve the revolution. It emerged because the revolution created requirements that the previous financial system could not meet.

The AI economy creates specific financial demands that legacy infrastructure is poorly positioned to serve. Micropayments at scale for AI API access, where a single user session may involve thousands of small transactions, are not compatible with card network economics. Autonomous agent transactions, where AI systems execute purchases and payments without human approval at each step, require programmable financial infrastructure with no dependence on human intermediation. Globally distributed AI workloads, where compute is purchased across multiple jurisdictions simultaneously, require borderless capital flows that settle in seconds rather than days.

AI agents are the next significant shift in how AI capability is deployed at scale. An AI agent executing tasks autonomously across multiple services and vendors needs a payment rail that operates without friction, at the speed of software, across jurisdictions. That is not a wire transfer. It is not a card payment. The financial infrastructure best positioned to serve this is being built on public blockchain networks. This is not a prediction about crypto speculation. It is a structural observation about what the AI economy’s financial layer needs to look like.

For those interested in how this convergence is already playing out in trading markets, a detailed examination of how AI is changing crypto trading right now covers the specific tools and approaches already available to active traders.

The broader point for investors is this. Platforms at the intersection of AI tools and crypto trading are positioned at the junction of both shifts. Copy trading as AI-era democratised investing represents one version of this: elite strategy performance made accessible to retail participants through platform infrastructure, without requiring the quantitative expertise those strategies were originally built on. That is itself a product of the AI era: the democratisation of capability through software that does the complex work for the user.

Trade the AI Economy

BingX combines copy trading that mirrors elite strategies with grid bots that automate market-neutral positions. AI-era tools, available now, without requiring a quantitative background.

Start Trading on BingXWhat Digital Investors Should Do Now

The fourth industrial revolution does not require retail investors to develop views on semiconductor geopolitics or pick individual AI stocks. A practical framework for thinking about positioning:

5-Point Framework

1

Foundation

Understand the infrastructure layer

Know who the compute and energy builders are and why infrastructure wins first in every industrial revolution. This context prevents the most common mistake: confusing application-layer product announcements with infrastructure-layer value creation. Not all “AI companies” are at the same layer.

2

Application Layer

Treat applications as early and high-risk

The dominant AI applications of 2035 may not yet exist as public investment opportunities. Concentration in early-stage application bets carries the same risk profile as internet stock-picking in 1998: some picks will be extraordinary, most will not survive. Diversification matters.

3

Digital Assets

Digital assets are the AI economy’s financial infrastructure

The demand logic is structural, not speculative. AI agents need programmable money. Borderless AI workloads need borderless capital. Micropayment-scale AI API economics need infrastructure that scales at software cost, not card-network cost. These are directional outcomes of how AI is already being deployed.

4

Practical Access

Use platforms that provide AI-era exposure without technical expertise

Copy trading and grid bots represent the democratisation of capability that the AI era makes possible. Choosing a platform for the AI economy is a concrete first step, not an abstract one.

5

Risk Management

Risk management is non-negotiable

Every industrial revolution produced major losers alongside major winners. Companies dominant in the railroad era were largely destroyed by the automobile era. Position sizing and diversification are not conservative choices — they are structurally correct choices in periods of deep technological transition.

Historical Precedent — Investors Who Acted on Structural Forces

Railroad Era

1830s–1880s

Electricity Era

1880s–1930s

Internet Era

1990s–2010s

AI Era

Now

The investors who positioned for each era did not wait for certainty. They positioned on the basis of structural forces that were visible, and were right about the direction even when wrong about the specific winners. The window for understanding the fourth industrial revolution before consensus catches up is still open — but historical precedent suggests it has a finite duration.

Start with the right platform

Copy trading, grid bots, and AI-era exposure — without needing to be a quant.

Frequently Asked Questions

What is the fourth industrial revolution?

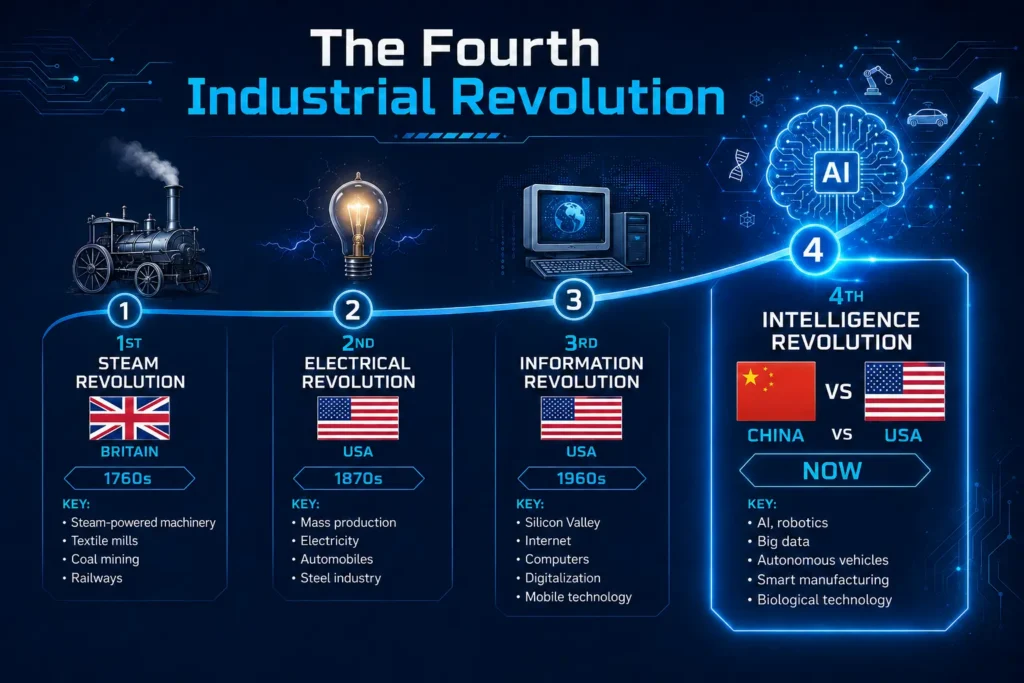

The fourth industrial revolution refers to the current structural convergence of artificial intelligence, advanced computing, and physical-digital systems that is reorganising how economic value is created. The first industrial revolution was steam and railways (1760-1840). The second was electricity, steel, and oil (1870-1914). The third was transistors, computers, and the internet (1960-2000). The fourth, beginning roughly in 2020, is built on AI, large-scale data processing, and the fusion of digital systems with physical infrastructure including robotics, autonomous vehicles, and smart cities. Unlike previous revolutions, it requires physical capital at extraordinary scale: frontier AI model training requires tens of thousands of specialised GPUs running for months at a time.

Who is currently winning the AI race?

The United States leads in leading-edge semiconductor manufacturing capability (through TSMC, which serves NVIDIA and others), in frontier AI model development, and in the accumulation of AI research talent. China leads in AI application deployment at scale, in national coordination of AI investment (1 trillion yuan AI fund announced in 2024), and in the systematic construction of an AI-ready workforce through its national education curriculum. The chip gap created by US export controls is real: Chinese AI labs train frontier models with Huawei Ascend hardware and older NVIDIA chips, at higher cost and longer timelines than their US counterparts. The capability gap is narrower than the chip gap alone would predict, because Chinese labs have adapted effectively to constrained compute. The race is not concluded.

Why does AI need so much energy?

Training a frontier AI model requires tens of thousands of high-performance GPUs running continuously for months, each consuming hundreds of watts of power. A single large training run consumes energy roughly equivalent to 300 transatlantic flights. Inference, meaning the deployment of trained models to serve user requests at scale, may ultimately consume more total energy than training as global AI deployment expands. The International Energy Agency projects that data centre electricity consumption could reach 1,000 terawatt-hours per year by 2026, roughly equivalent to Japan’s national electricity consumption, driven primarily by AI workloads. This has triggered investment in nuclear energy restarts (Microsoft’s Three Mile Island agreement), utility-scale solar, and long-duration energy storage that extends well beyond the technology sector.

How are NVIDIA and Huawei competing in AI chips?

NVIDIA holds approximately 70-80% market share in AI training hardware through its H100, H200, and B200 Blackwell GPU series, manufactured by TSMC at 3nm and 4nm. Its competitive depth includes both hardware performance and the CUDA software ecosystem, which all major AI training frameworks are built on. Switching away from NVIDIA requires rewriting the software stack from scratch. Huawei’s Ascend 910B chip achieves approximately 80% of H100 performance on certain benchmarks, manufactured by SMIC at 7nm. The 7nm-to-3nm manufacturing gap means Huawei cannot match NVIDIA’s performance per chip or energy efficiency. Chinese AI labs use Ascend and older NVIDIA hardware to train competitive models, but at higher cost and on longer timelines than US-aligned labs.

What does the fourth industrial revolution mean for crypto and digital assets?

The AI economy creates structural demand for financial infrastructure that legacy systems cannot efficiently serve: micropayments for AI API access at scale, autonomous agent transactions without human intermediation at every step, and borderless capital flows for globally distributed AI workloads. Public blockchain infrastructure is positioned to serve this demand because it is programmable, borderless, and operates without the intermediary costs of card networks or wire transfer systems. AI agents, which execute tasks autonomously across multiple services, require payment infrastructure that operates at the speed of software. That infrastructure is being built on crypto rails. The convergence is visible in the development roadmaps of major AI companies, though not yet at full deployment scale.

How can retail investors position for the AI economy?

Direct exposure to the AI infrastructure layer (NVIDIA, TSMC, major hyperscalers) is already priced at significant premiums in public markets. The application layer is early but requires deep sector knowledge to assess. A practical path for many retail investors runs through digital assets and crypto trading platforms that serve as the financial infrastructure layer of the AI economy. Platforms like BingX offer copy trading tools that allow retail participants to follow elite traders without requiring quantitative expertise, and grid trading bots that automate market-neutral strategies. These are AI-era tools: they democratise access to capability that previously required institutional resources. Register on BingX to access these tools with an exclusive welcome reward.

Is AI a threat to employment or an opportunity?

The framing of AI versus human employment misses the more relevant question: which humans will direct AI systems, and which will capture the value those systems create? Every major industrial revolution displaced categories of work while creating new ones. The net employment effect of the first, second, and third industrial revolutions was positive over 20-30 year periods, while being highly disruptive in 5-10 year windows for specific industries and geographies. The relevant distinction in the AI era is between people capable of directing AI systems effectively and people who cannot. Every employee will eventually manage AI workers in some capacity. Building that capability before the displacement pressure arrives, rather than after, is the practical response. Countries building this into their education systems now, as China is doing systematically through its AI curriculum mandate, are accumulating a structural workforce advantage that compounds over decades.

Vanessa Chen

Intelligence and AI Economy Analyst, BusinessCommunity.ai

Vanessa covers the intersection of artificial intelligence, digital finance, and infrastructure geopolitics. Her work focuses on the structural forces reshaping global wealth creation and what they mean for investors positioned at the AI-crypto convergence.

Cryptocurrency trading involves significant risk and may not be suitable for all investors. This article is for informational purposes only and does not constitute financial or investment advice. Past performance is not indicative of future results. Always conduct your own research before making any investment decisions.